How healthy are Britain's banks?

AFP

AFPThe Bank of England will announce on Wednesday the strength of the UK's biggest lenders ahead of Brexit.

The Bank of England devises hypothetical scenarios for the economy, house prices and interest rates, which are designed to put pressure on the banking system.

The results of the stress tests will be published on 28 November at 16:30 GMT.

The Bank will also publish an assessment of the Brexit deal on its operations.

What are the stress tests?

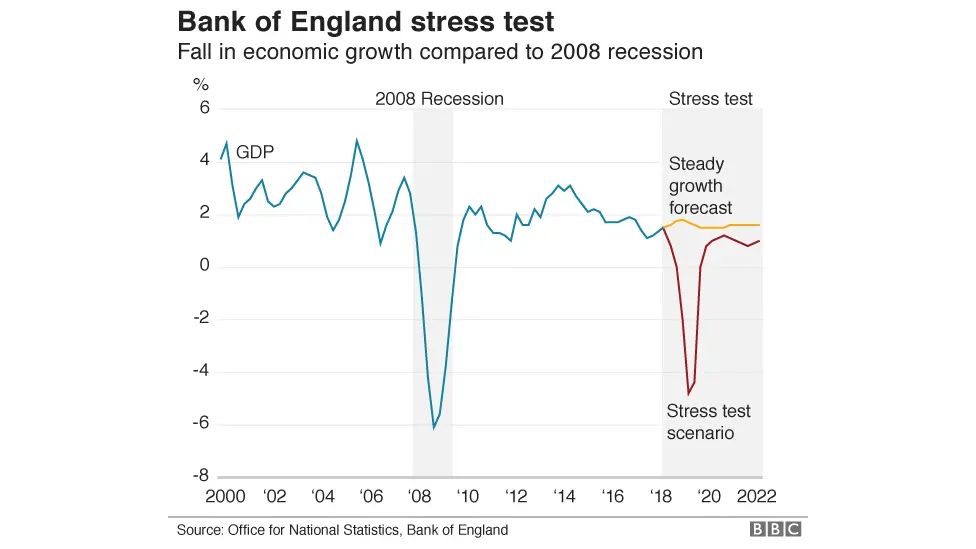

The tests - a health check on the financial system - have been conducted annually since 2014.

They are born out of the financial crisis, when banks financial strength was severely tested and left taxpayers to rescue Royal Bank of Scotland and Lloyds Banking Group.

The banks also stopped lending to households and businesses.

Ian Gordon, banks analyst at Investec, said the stress tests are more severe than the 2008-2009 crisis and designed to check banks still have enough capital to meet current financial rules.

What is in this year's tests?

The Bank of England published the scenarios for this year's stress tests in March.

They were largely similar to the previous year, when the Bank of England said that banks could handle a "disorderly" Brexit.

AFP

AFPThe Bank of England uses the following scenarios over a five-year period:

- 33% fall in property prices

- a 40% fall in commercial property prices

- Unemployment peaking at 9.5%

- UK GDP falling by 4.7%

- World GDP falling by 2.4%

- The interest rate rises to 4%

The Bank of England says these scenarios are comparable to, or more severe than the financial crisis.

Which banks are tested?

The impact on the financial strength of each of the major UK-based banks is expected to be published.

They are Barclays, Lloyds Banking Group, HSBC, Santander and the Royal Bank of Scotland.

London-based Standard Chartered is also included, as is the Nationwide Building Society.

What happens if they fail?

The Bank of England sets each bank its own hurdle rate.

It also wants make sure the banking sector can keep increasing lending to households and businesses by 2% under the stress scenario.

If this is impeded, the bank could be forced to hold back dividends to shareholders, or even ask them to back a fund-raising effort to boost their capital position.

This year's results could differ from last year's because of new accounting rules, which mean banks must start putting money aside against their bad debts much earlier.

"We may see quite different results to the same shock scenarios from 12 months ago as banks deal with the new rules," said Dan Cooper, Head of Banking in the UK at accountants EY.

What will the experts look for?

The financial dent on each bank will be closely analysed by investors for clues to their ability to pay dividends in the future.

But the market will also be looking at the bank's half-yearly assessment of risks to the financial system.

Getty Images

Getty ImagesIn its last assessment in June, it warned about the risk to trillions of pounds of financial contracts that could be posed by Brexit.

And much of the focus will be on the Bank of England's analysis of how the Brexit deal will affect its ability to deliver its statutory remits for monetary and financial stability.

This will also include a "no deal, no transition" scenario.

This was requested by the Treasury Committee in the summer.

MPs asked for it to be provided after the negotiations between the government and European Commission concluded, but before any parliamentary vote.

That vote is scheduled for 11 December.

The Bank of England pulled forward the publication of the stress tests results by one week to Wednesday to accommodate this request.

It surprised the markets today by announcing that the publication of the results would be delayed by nine hours from from 07:00 tomorrow to 16:30 instead, which pulled down the share prices of banks.

Mr Gordon said this was because there was some speculation that banks might be required to bolster their capital, temporarily, in advance of Brexit.