Surge in ultra-long mortgages among under-30s

Getty Images

Getty ImagesHundreds of thousands of homeowners have taken out mortgages in the last three years that they will still be paying off into retirement, estimates suggest.

A surge in mortgage terms beyond state pension age has been seen, particularly in new home loans made to the under-30s.

Figures from the Bank of England show how the share of new mortgages with a later end date has increased.

Higher mortgage rates have led many people to choose an extended repayment period to control costs.

However, as they will be paying off their mortgage for longer, they will pay more interest so the overall cost is likely to be higher.

The figures emerged from a Freedom of Information (FoI) request made by Sir Steve Webb, a former pensions minister who is now a partner at pensions consultancy LCP.

"The challenge of getting on the housing ladder is forcing large numbers of young home buyers to gamble with their retirement prospects by taking on ultra-long mortgages," he said.

He suggested that using limited retirement savings to clear a mortgage could leave people at greater risk of poverty in old age.

While many young homeowners have chosen longer mortgage terms to make repayments more manageable, they may opt for shorter terms in the future if their salaries improve or they move house.

How long such a trend might last will also depend significantly on whether mortgage rates drop and settle.

The FoI request followed a Bank of England financial policy report that included mortgage data for the fourth quarter of 2023. Mr Webb requested the corresponding data for the fourth quarter of the previous two years.

The Bank of England's data shows that in the final three months of 2021, some 31% of new mortgages had an end date beyond state pension age.

Two years later, some 42% of new mortgages had this end date during retirement, suggesting a rise in popularity of longer-term loans.

Across the final quarters of all three years, nearly 300,000 new mortgages were in this category.

A considerable amount can change in homeowners' financial prospects during their working lives.

A longer-term mortgage may be replaced by a shorter-term one as someone's income rises, or they find other ways to pay off their mortgage.

However, the pressure on young homeowners is clear with a sharp rise in the proportion of mortgages that run beyond pension age.

The number of homeowners aged under 30 taking out such mortgages more than doubled over the two-year period, while for those aged under 40 the number was up 30%.

Meanwhile, older age groups saw a decline in such mortgage deals.

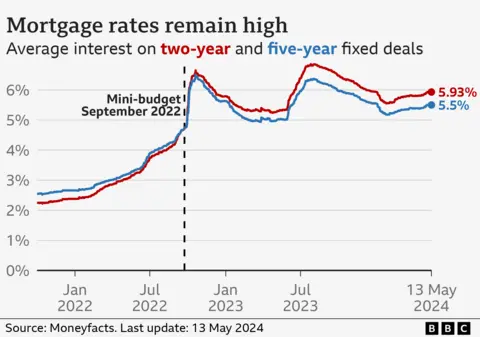

That has occurred during two years of upheaval in the mortgage market. Rates are much higher now than they were at the end of 2021.

On Thursday, while holding the base rate at 5.25%, the Bank of England edged towards a rate cut in the summer and hinted at further cuts.

The Bank's governor, Andrew Bailey, said he was "optimistic that things are moving in the right direction" regarding the UK economy, leading to speculation of base rate cuts.

Ways to make your mortgage more affordable

- Make overpayments. If you still have some time on a low fixed-rate deal, you might be able to pay more now to save later.

- Move to an interest-only mortgage. It can keep your monthly payments affordable although you won't be paying off the debt accrued when purchasing your house.

- Extend the life of your mortgage. The typical mortgage term is 25 years, but 30 and even 40-year terms are now available.